How the de-carbonisation agenda and the reduction of CAPEX drives forward deployment of RE in Europe

by Ypatios Moysiadis

Regardless whether you believe in the future of renewable energy, it is an undeniable fact that solar and wind have established themselves as mainstream generating technologies across the globe.

More and more often we see records being broken and whole countries running for consecutive weeks on green energy alone. The UK, for example, ran for a fortnight without burning any coal for electricity breaking a national record earlier this year.

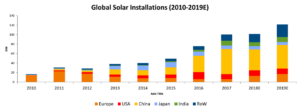

China is the steam engine in this global transformation with Europe, US and India following behind.

Source: BNEF

Global Energy Investment changes

A closer examination of the global clean energy investment and capacity installations from 2010 onwards will reveal that even though for the last 8 years total investments remained relatively stable, we managed to install more capacity reaching 179 GW (including hydro) in 2018, according to IRENA and BNEF.

This reflects mainly the massive drop in CAPEX evolution, both in solar and wind, the development of more dynamic business models (based on corporate PPAs and direct sale to the retail markets) and the entry of mainstream Utilities and Oil Majors in the industry.

However, it would be naïve not to recognise some key factors driving this change outside the industry.

So, what drives the change?

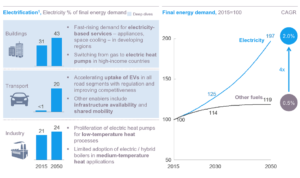

Increased Demand – Electrification of our Society

All societies electricity demand will significantly increase over the next decade.

Housing stock and buildings will be required to switch from gas to electric heating systems and temperature rise due to climate change will result in the need for electric-based cooling systems even in northern regions.

The electrification of our transportation system from vehicles to planes and ships will demand a different electric grid with more flexible energy management and power flow.

The industry, driven mainly by the need to identify efficiencies, will reduce risk (polluters will pay) and adoption of new standards will follow this trend.

Environmental agenda

For years environmental and social issues were a secondary concern. Today we see a massive shift both in enterprises and consumers. Corporates are forced to consider the environmental and social impact of their assets and their operations. Consumers and especially those belonging to Generation Y (Millennials) and Gen X become prosumers. They are aware, informed and can very quickly self-organise putting pressure on both corporate and political agendas.

Technology – Value shifts downstream

Technology works as an enabler shifting value downstream to consumers. Value is shifted from conventional generation at utility-scale, downwards to grid transmission and distribution, to aggregated virtual trading and finally to distributed flexible generation and energy services platforms. Grid-connected EVs, residential PV and battery systems will form part of the wider energy management services and a new interactive mode of operation.

Geo-Economics

Europe has taken a strategic decision to reduce its dependency on oil & gas imports from countries outside the EU. Following the decision to decommission coal and nuclear stations, the only alternative is to invest further in large scale renewables.

The current trends and spot markets: Renewables Energy

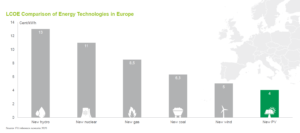

The massive reduction in CAPEX and increase in efficiency allow renewable energy projects and especially solar PV to be developed in a subsidy-free environment. The reality is that new Solar PV provides the lowest LCOE of any other generating technology. Furthermore, the carbon neutrality bill in the EU supported by many EU countries is creating a favourable environment for green energy production.

These factors have encouraged the resurrection of many European markets which can capitalise on high irradiation or wind yield.

Traditional markets like Germany and France have continued to steadily increase installed capacity. However, more countries have established mechanisms allowing the development of more Renewable energy projects. A closer examination of some spot markets is revealing of current trends.

Spain – Aims to fully decarbonise its energy generation by 2050. With a very ambitious plan, the country aims to install 3GW of wind and solar energy every year for the next 10 years. Over the last few years, we have witnessed an influx of new big projects and hundred of MW in development from a wide range of different developers. However, this “gold rush” is driven by PPAs and this exactly is where the risk is. The market can get easily “overheated” with speculation and capacity hoarding. Therefore, many investors are taking a more conservative approach to the Spanish market.

Portugal – The country aims to cover 80% of its energy demand with Renewable Energy by 2030 and electrify 65% of its economy, achieving carbon neutrality by 2050. The country prepared and launched a 1.75GW auction with the results published early August. Furthermore, Portugal will invest €474m into grid expansion and re-enforcement.

Italy – Following the National Renewable Energy Action Plan, Italy is gearing up to launch 7 renewable energy auctions. The first 500MW is planned for the 30th of September 2019. The overall plan is to add 4.8GW of additional green energy in the next 2 years.

Greece – Following the stabilisation of the economic conditions and the positive growth outlook in 2018, Greece decided to run annual CFD-like auctions both technology-specific and mixed. The country aims to tender 430MW and 300MW in 2019 and 2020 on technology pots and another 500MW on technology-agnostic auctions.

New Business Models

The awakening of both the Oils Majors and the Utility companies has brought different vertically integrated business models into the market. Both are addressing the more aware retail market, which is willing to pay more for sustainable energy and this is creating new market dynamics. Companies like Shell and BP are investing not only in generating assets but also in new innovative technologies across the cleantech board (from batteries to “smart” trading and EVs).

This new competitive environment puts enormous pressure into the more traditional IPPs which were the drivers of both the industry and the RE expansion to date. However, it is an undeniable testament to the fact that the industry is transforming and maturing.

Europe has a unique opportunity to be at the forefront of the de-carbonisation agenda and lead the way to carbon neutrality. Investment on advanced analytics, AI and services innovation, will drive forward further cheaper deployment of RE by capitalising on data and by transforming the grid.

For more visit my Youtube Channel or continue reading the Cleantech Geek Blog.